Getty’s SPAC Deal is Two Decades in the Making

The Rundown - Your weekly SPAC Deep Dive (02/10/22)

Hey Guys!

With over 415 million assets, 340,000 contributors and nearly $1 Billion in annual revenues, Seattle-based Getty Images may be the most dominant company in the stock photography industry. After being in private-equity hell for the better part of the last decade, the company is finally making a return to the public markets through a $4.8 Billion SPAC deal with CC Neuberger. Getty has been plagued with challenges including Corporate Mismanagement, Rising Debt & Competition from Low End/Mobile Studios.

However, things are finally looking up for the company, on the back of fresh investment from the founding family, increased spending to keep the innovation wheels spinning & strategic acquisitions to become the industry leader yet again. With all of this in mind, what does the future hold for Getty and the potential SPAC Investors?

From London to Seattle

To understand Getty’s current business trajectory, we need to look back to the original vision of the company. Mark Getty and Jonathan Klein co-founded Getty Communications, in a bid to disrupt the stock photography industry. The co-founders noticed that the market was highly fragmented and inefficient, with mostly small agencies selling premium photos in exchange for hundreds (thousands in some cases) of dollars while splitting the profits with photographers. The company commenced operations in 1995 by purchasing Tony Stone Images, which was one of the largest providers of contemporary stock photography with over one million photographs and $42 million in annual revenues.

Getty’s strategy was to become a market leader in the space through consolidation, which relied on a series of acquisitions. In the late 90s, the company started aggressively pursuing acquisition in the private stock photography space. This included the acquisition of Archival Photography Company Hulton Deutsch (1996), Contemporary Photo Firm Fabulous Footage and Photography Agency Liaison. In 1997, Getty Merged with PhotoDisc to create Getty Images.

With the inception of the Dotcom era and the rise of digital distribution in the photography space, Getty signed a distribution agreement with IBM. During this period, the company also went public through a Nasdaq listing & moved its headquarters to Seattle. By 2006, the firm had over 2,000 employees with offices in New York & London, generating more than $130 million in the bottom line. Getty started facing fierce competition from low-end agencies on the market, such as iStockPhoto, which was selling low-quality photos for as little $5-$10. With competitors eating into the company’s market shares, the founders decided to take sell their stake in the company. Getty was sold to private equity firm Hellman & Friedman for $2.4 billion in 2008, and later in 2014 by Carlyle for $3.3 Billion.

Sponsored this week by…

Want to Find the Best SPACs? Try Benzinga

(Offer Expires 2-14-2022)

I use tons of trading software to help me better understand the market and make smarter trading decisions. One thing I love about Benzinga Pro is its versatility. It wasn’t built for just one type of trader but for a wide range of experienced investors like myself. I can create custom watchlists, and then quickly monitor the performance of my investments.

Some great news - Benzinga is giving all subspac readers a free two week trial!

The Private Equity Era

While the private equity era was meant to usher a turnaround for the company by becoming the dominant player once again, several challenges plagued Getty. When Carlyle financed the takeover of the company from Hellman & Friedman, it did so primarily through debt ($2.6 billion of the $3.3 billion), which was reflected on Getty’s balance sheet. As a result of the increased debt load, a majority of the firm’s cash flow now went to service the debt and pay dividends to investors, resulting in very little CapEx & R&D spending. As a result, the company was left behind by competitors who were prioritising growth at the time through investments in new technologies.

Getty’s challenges broadened in the smartphone photography era, where the supply of new photos and videos exponentially outpaced what distributors could charge for each one. Over the last three decades, the volume of licensed images distributed by the company has grown a hundredfold, but revenues haven’t kept up (revenues have roughly 3x during the period). With technology and pressure from competition driving down costs significantly during the period, customers looked for the cheapest creative solutions. To compensate, the company’s in the stock photo industry had little choice but to boost volume while keeping costs low. The ensuing race to the bottom resulted in both revenues & operating margins shrinking.

Return of Getty & A Business Turnaround

With Carlyle struggling with the Investment, the Getty Family re-entered the fray in 2018, to acquire a majority stake in the firm in 2018. The family rolled over the $2.35 billion in debt from Carlyle, while investing $250 million for Carlyle’s state. The new management rolled out a host of technological initiatives to turn around the business, including revamping its distribution platform, improving search across its platform and adjusting image searches to improve the ratio of historically underrepresented stock subjects.

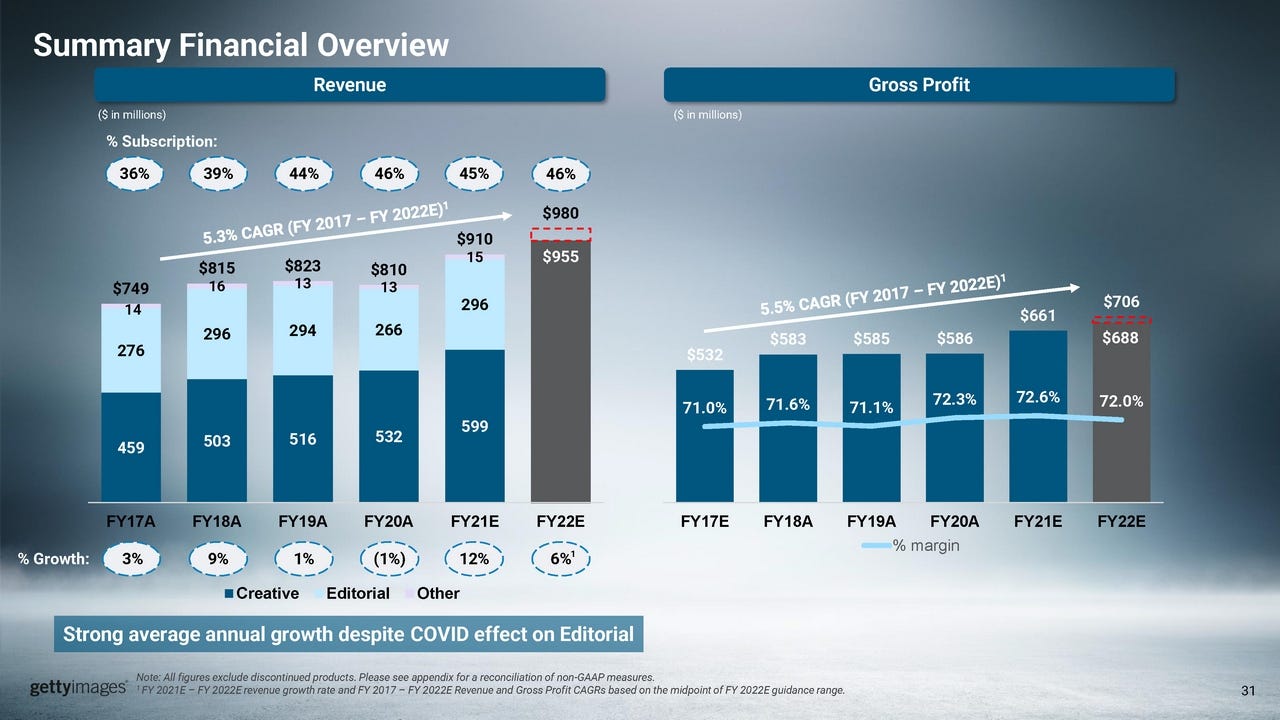

Perhaps the largest and most important transition came when the company decided to transition all of its creative stock photography offerings from a Rights Managed Licence to a Royalty Free Licensing Model. With creative use cases for stock photography now primarily revolving around digital marketing, customers needs are better met through the Royalty Free Model. With the rollout of the new model, Getty’s revenues & Gross margins subsequently improved compared to prior years (12% revenue growth, 200 bps gross margin expansion).

The SPAC Deal & Avenues for Future Growth

Getty announced plans to go public through a SPAC merger with CC Neuberger Principal Holdings II in a $4.8 Billion Deal. The deal represents a 15.2.x Froward EBITDA Multiple (EBITDA estimated to be $315 million), indicating that management sees itself as a mature business. The deal is expected to infuse the company with nearly $1.1 Billion in Cash, most of which will be used to pay off the company’s existing debt (which has been problematic for the company in the past). The current addressable market for Getty is estimated to be $3.3 billion and grow to $4.8 billion by 2028.

While Getty’s growth has been slow over the last few years due to a shutdown of entertainment & sports, the company expects revenues to bounce back as a result of several catalysts. This includes a rebound in the Sports Market, Growth Across the Video Market & the Company’s entry into the NFT Market. For the first time in its history, the company has a division for each segment of the population, with GettyImages targeting the enterprise market, iStock targeting Small and Medium Businesses and Unsplash targeting semi-professional creators.

Bottom Line

Throughout the Last Two and a Half Decades, Getty Images has seen its business see-saw between being the industry leader & disruptor to being Irrelevant. Rising debt levels, mismanagement & high competition from low-end photo studios hampered the company for the better part of the last decade. However, with the return of the Getty Family, an increase in CapEx & technology spending, in addition to key strategic acquisitions has once again given the company its leadership position. While the overall trajectory of the industry remains in question, Getty seems well-positioned to capture most of the future growth.